In our second instalment on capital adequacy regulations for US financial institutions, we look at the credit risk requirements under the internal ratings based (IRB) and advanced measurement approaches (AMA). Earlier we had reviewed eligible capital, minimum capital ratios as well as risk weights under the standardized approach for credit risk. In this post, we begin by looking at which institutions would qualify for using the IRB & AMA approaches for assessing credit risk for capital adequacy purposes. Then we look at the minimum criteria that must be met before institutions are permitted to use these measurement methods for calculating their capital requirements for credit risk. The criteria covers various facets of the institution, including its processes, systems, segmentation methods, parameter quantification approaches, model use, data management & maintenance, controls and documentation. Finally we see how capital requirements and risk weighted assets are determined under these approaches for different types of exposure.

Applicability & minimum qualifying criteria

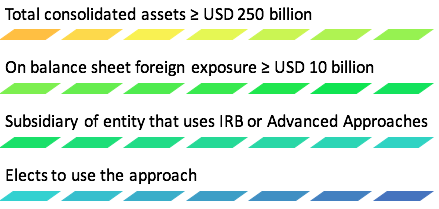

Applicability criteria

The IRB and advanced measurement approaches are applicable to the following financial institutions:

Minimum qualifying criteria

To be able to use these approaches institutions must meet the following minimum qualifying criteria on an on-going basis. The minimum qualifying criteria address the following categories:

Minimum criteria for process & systems include:

- Assess and maintain adequate capital in relation to risk profile

- Consistent with internal risk management and MIS processes & systems

- Risk parameters & data used should be consistent with the institution’s own credit & operational risk exposures

Minimum criteria for risk rating & segmentation include:

- Differentiate between whole sale and retail exposures

- Reliable internal risk rating system & a loss severity rating grade system for wholesale exposures

- For retail exposures, an internal system that groups exposures by subcategory and segments each subcategory for PD and LGD estimates

- Choice of business, economic and industry conditions should impact obligor rating assignments for wholesale exposures

- Review & update whole sale exposures obligor and loss severity ratings whenever new information is available or at least once a year

Minimum criteria for risk parameter quantification include:

- Comprehensive process for determining accurate, timely and reliable estimates

- Data of sufficient quality and relevance

- Conservative estimates when relevant data is limited

- Should not factor in US government financial assistance unless explicit legal commitment is present

- Historical experience of the bank’s ability to reduce its exposure to troubled obligors prior to default must be present if LGD estimates consider such effectiveness

- For PD estimates ≥ 5 years of default data is required

- For LGD & EAD estimates for wholesale exposures ≥ 7 years of loss severity & exposure amount data is required

- For LGD & EAD estimates for retail exposures ≥ 5 years of loss severity & exposure amount data is required

- Data must include periods of downturn. If not available, parameter estimates need to be adjusted.

- PD, LGD & EAD estimates must be based on the definition of default

- Periodic review of reference data to assess relevance, quality & consistency with default definition

Prior written approvals are required for the use of the following models:

- Counterparty credit risk model

- Double default treatment

- Equity exposures model

Minimum criteria for operational risk include:

- Independent management function, process document & MIS system, operating risk data and assessment systems & risk quantification systems

Minimum criteria for data management & maintenance include:

- Support advanced systems and timely & accurate reporting

- Data retained electronically for timely retrieval for analysis, validation, reporting, and disclosure purposes

- Key risk drivers captured for adequate monitoring, validation, and refinement of its advanced systems

Minimum criteria for control, oversight & validation mechanisms include:

- Senior management to ensure that advanced systems function effectively

- Annual review & approval of advanced systems by Board of Directors

- Effective system of controls and oversight

- On going validation of advanced systems

- Independent internal audit function

- Periodic stress tests of advanced systems

Minimum criteria for Documentation include:

- Document all material aspects of the advanced systems

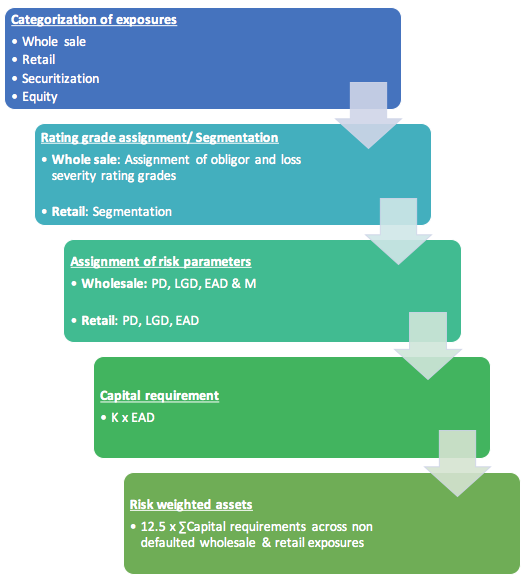

Risk weighted assets for general credit risk

Non defaulted whole sale & retail exposures

The process followed for calculating credit risk weighted assets for non-defaulted whole sale and retail exposures is given below:

- Retail categorization includes three subcategories – residential mortgage exposure, qualified revolving exposure and other retail exposure

- Whole sale categorization includes a number of subcategories such as high volatility commercial real estate (HVCRE) exposures, whole sale exposures, sovereign exposures, OTC derivative contracts, repo style transactions, eligible purchased whole sale exposures, eligible margin loans, clear transactions, default fund contributions, unsettled transactions, eligible guarantees or eligible credit derivatives.

- For most cases, PD cannot be less than 0.03%, LGD cannot be less than 10% and M, the effective maturity must be greater than or equal to 1 year and less than equal to 5 years.

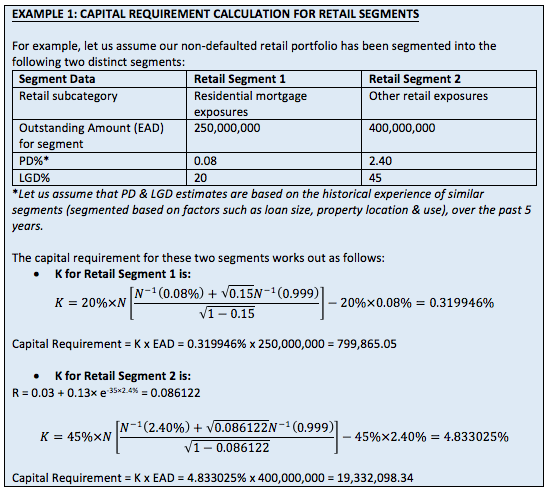

The capital requirements, K, for non-defaulted retail and wholesale exposures are as follows:

- K for retail exposures:

Where

R = 0.15 for residential mortgage exposures

R = 0.04 for qualifying revolving exposures

R = 0.03 + 0.13 × e-35×PD for other retail exposures

Note:

For PD = 0, K= 0.

N(.) is the cumulative distribution function for a standard normal random variable, NORMSDIST(.) function in EXCEL.

N-1(.) is the inverse cumulative distribution function for a standard normal random variable, NORMSINV(.) function in EXCEL.

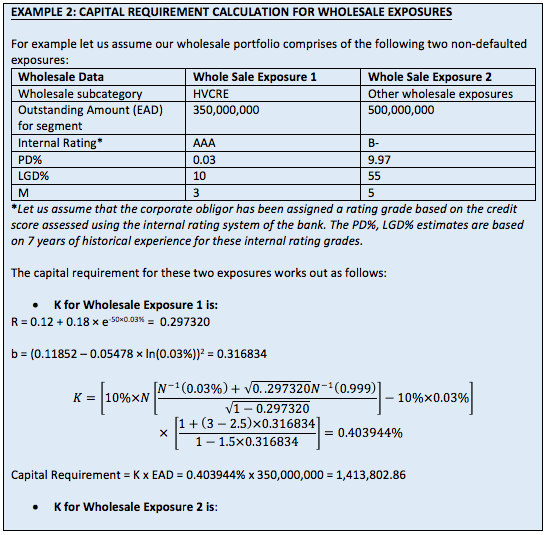

- K for wholesale exposures:

Where

R = 0.12 + 0.18 × e-50×PD for HVCRE exposures

R = 1.25 × (0.12 + 0.12 × e-50×PD) for unregulated financial institution exposures & exposures to regulated financial institutions with total assets ≥ USD 100 billion

R = 0.12 + 0.12 × e-50×PD for other wholesale exposures

b = (0.11852 – 0.05478 × ln(PD))2

Note:

For PD = 0, K= 0.

N(.) is the cumulative distribution function for a standard normal random variable

N-1(.) is the inverse cumulative distribution function for a standard normal random variable

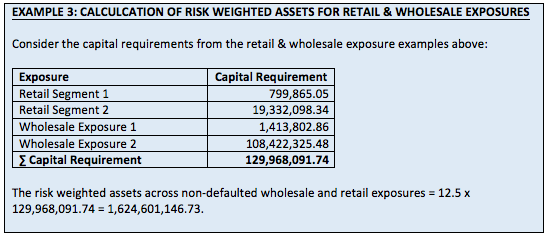

Risk weighted assets = 12.5 × Capital Requirement, where Capital Requirement is summed across all non-defaulted wholesale and retail exposures.

Defaulted whole sale & retail exposures

The capital requirements for these exposures is given below and depends on whether or not the exposure is covered by an eligible US government guarantee:

- If the entire exposure is not covered by the guarantee, the capital requirement will equal 0.08 × EAD

- If a portion of the exposure is covered by the guarantee, the covered exposure will have a capital requirement of 0.016 × EAD while the portion of the exposure that is not covered will have a capital requirement of 0.08 × EAD.

Risk weighted assets = 12.5 × Capital Requirement, where Capital Requirement is summed across all defaulted wholesale and retail exposures.

Assets not included in a defined exposure category & non material portfolio exposures

These exposures will be treated as follows:

| Asset | Treatment |

| Cash owned, held in supervised institutions offices or in transit | Risk weighted asset = 0 |

| Gold bullion assets held in own vaults or in another depository institutions vaults

(net of gold bullion liabilities) |

Risk weighted asset = 0 |

| Cash items in the process of collection | Risk weighted asset = 20% of carrying value |

| Pre-sold construction loan | If purchase contract in effect, risk weighted asset = 50% of carrying value

If purchase contract cancelled, risk weighted asset = 100% of carrying value |

| Retail lease exposure | Risk weighted asset = Residual value of exposure |

| DTAs arising from temporary differences that the institution could be realized through net operating loss carry backs | Risk weighted asset = carrying value |

| MSAs, DTAs arising from temporary differences that the institution could not be realized through net operating loss carry backs & significant investments in the capital of unconsolidated financial institutions in the form of common stock that are not deducted for regulatory capital purposes | Risk weighted asset = 250% of exposure amount not deducted for regulatory capital purposes |

| Any other on-balance sheet asset that is not a wholesale, retail, securitization, IMM, or equity exposure, cleared transaction, or default fund contribution and is not subject to deduction | Risk weighted asset = carrying value |

| Non material portfolio exposures | If on balance sheet exposures, risk weighted asset = carry value

If off balance sheet exposure, risk weighted asset = notional amount |